Nobel Laureate Joseph Stiglitz argues that Gross Domestic Product (GDP) is no longer the right measure for success, and provides compelling reasons for why the GDP measure alone is not complete. Depending primarily on this measure is akin to a doctor depending primarily on the weight of a patient to assess the patient’s health. Things might look good from the outside, but the patient might be dealing with major illnesses that weight alone cannot highlight. So it is with GDP—while countries might experience an increase in GDP, the metric fails to highlight major problems with the economy.

But considering that GDP is still the most used measure to assess the economic health of a country, many governments and development organizations work hard to boost the GDP of poor countries. And they do so by using levers such as raising or lowering interest rates, boosting government spending, providing stimulus to boost consumption, and several others. Given this context, this blog provides a simple explanation of GDP that can help governments and development officials focus their efforts on supporting the vibrancy of firms—the most important driver of GDP.

Understanding GDP

A nation’s GDP is the market value of all the goods and services produced in the country. It is typically measured on an annual basis and an increase in GDP indicates that the economy is growing. During the Great Depression or the Great Recession in 2007 through 2009, for instance, GDP in the United States shrank, implying a slowdown in economic growth.

Economists assert that economic growth comes from three sources: increases in labor, increases in capital, and increases in efficiency with which labor and capital are used. But in order to get an increase in any of the sources of growth outlined above, someone has to make a decision to invest. And in a capitalistic economy, it is primarily managers in companies that do the investing, not governments. So, if managers choose to invest, then the economy grows. However, if they don’t, it slows.

Going a bit deeper: the GDP equation

A deeper observation of the individual components that make up the GDP shows how important managers’ decisions are to GDP growth. Mathematically, GDP is defined as:

C + I + G + X – M

where,

C = Consumption by households

I = Investment in productive assets

G = Government spending on goods and services

X = Exports

M = Imports

Now let us consider each of the components in the equation.

Each component in the GDP equation is directly tied to the vibrancy of firms or enterprises in a given country. Consider consumption which, at first glance, seems more related to individuals than enterprise. But households can only consume if individuals in the households have income, which typically comes from employment. If companies are not hiring or investing, then individuals will not be consuming much because they will not have the income to do so. This is one of the reasons why jobless countries have low GDPs—very few people have income to spend.

The next component in the equation, investment, refers to companies’ expenditures on capital equipment, fixed structure, software, and inventory. These investments are geared towards increasing the future output of final goods and services. They can also include wages and salaries paid to people as part of an investment project. If the enterprises are not investing, this number goes down, thereby pulling GDP down with it.

Now we consider government spending, which represents the amount of monies the government spends on goods and services. Since most governments do not technically create anything, they have two primary sources of revenue which they use for expenditure: taxes (these includes fines, licenses, permits, and fees for government services) and borrowing.

The government’s income is directly dependent on the success of firms, since corporations cannot pay taxes when they are not making money. Further, personal taxes and investment taxes come from income which we know results from productive enterprises. In the case of borrowing, countries with vibrant enterprises are more likely to receive better borrowing terms because their governments are in a better position to pay back the loans through taxes on their citizens or enterprises. There is a reason the United States can borrow money at near zero percent while Venezuela’s borrowing rates can be as high as 50 percent.

The next two components, exports and imports, don’t need much of an explanation regarding their relevance to enterprise. Enterprises make the goods that end up being exported and imported.

Where does that leave us?

Breaking down the GDP in this fashion may seem too simplistic, but often times, simplification gets us back to the basics. While monetary policy, fiscal policy, tax policy, and several other measures employed by governments to spur economic growth are important, at the core, if enterprises are not investing in innovations that spur consumption and create jobs, economic growth will remain tepid.

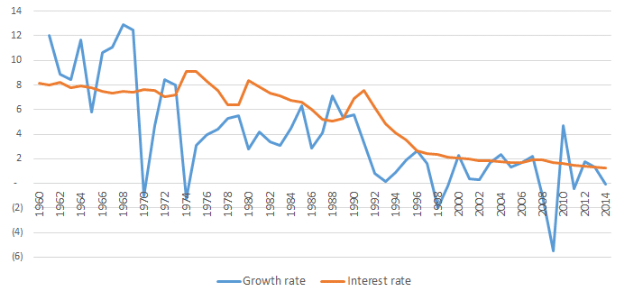

Consider the Japanese economy which grew, on average, at a breakneck pace of 6.15 percent from 1960 to 1990 during which time it had an average interest rate of 7.3 percent. From 1990 to today, the economy has grown, again on average, at a rate of approximately 0.9 percent, despite the country having decreased its interest rate to an average 2.5%. Today, the interest rate is actually zero percent, but Japan’s growth continues to progress at a snail’s pace. Clearly, trying to stimulate the economy primarily by decreasing the interest rate is not working for Japan.

During the 1960s through the 1990s, when interest rates in Japan were very high relative to what they are today, many of Japan’s innovative companies developed products that targeted nonconsumption, Companies such as SONY, Toyota, and Honda are examples of those that targeted nonconsumption in their respective industries. Targeting consumers who were formerly unable to purchase a product is a proven way to fuel employment and productivity, thereby boosting GDP. Today, however, many Japanese companies are targeting wealthier consumers and markets which typically makes less of an impact on employment and growth.

Japan’s interest rate and growth rate, in percent, from 1960 to 2014.

Let the story of Japan be a cautionary tale that productive enterprise, and more specifically enterprises that target nonconsumption, are at the core of economic prosperity.

For more, see:

Crime will rise in African cities like Lagos, but we have the tools to stop it