I was fortunate to speak at the 2024 Africa Prosperity Summit in Lagos, Nigeria where I shared insights on the role of venture capital in not only solving many challenges Africa faces, but also creating sustainable prosperity on the continent. As I developed my presentation, the supreme importance of carefully and intelligently deploying venture capital in Africa became more apparent to me. Here are three insights I shared.

First, our modern day understanding of venture capital–defined as risk capital designed to fund the creation of ventures (typically companies) that solve problems in society–evolved to solve specific problems associated with deploying risk capital to create entrepreneurial ventures in the United States. It’s important to note that “venture capital” hasn’t looked the same in different economies. In some economies, the government had a heavy hand in leading where this venture capital flowed, while in others the government had a more laissez faire approach. In each case however, the function of venture capital remained the same: the deployment of risk capital to solve societal problems.

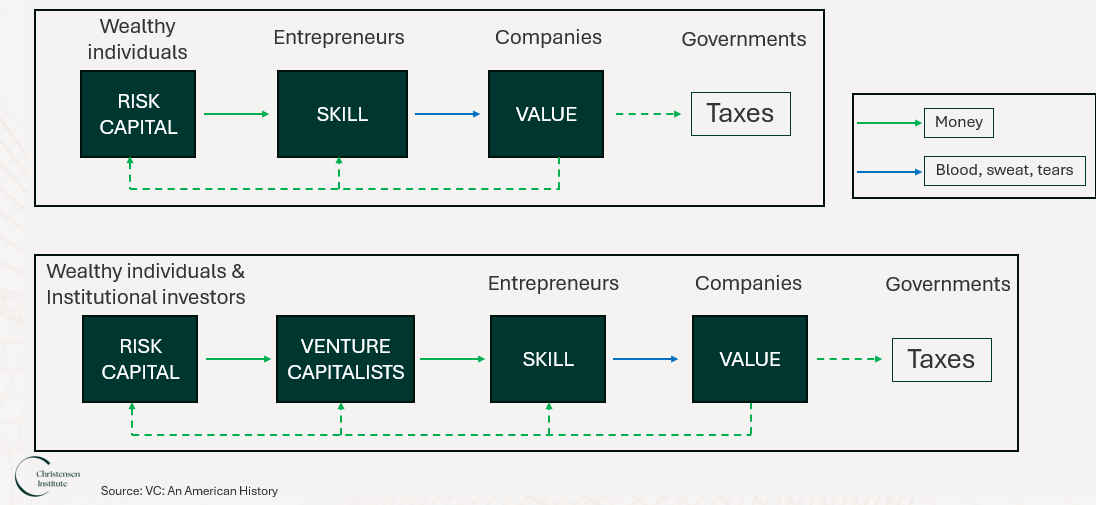

In the U.S., as is the case in every economy, there is often a huge gap between holders of capital and the people with entrepreneurial skill necessary to create value for people. This gap is characterized by risk: a lack of trust, fraud, and opacity. Historically, it was the job of wealthy individuals to deploy this capital to entrepreneurs who would then create value. In turn, some of the financial returns from the value created would flow back to the entrepreneurs, the government, and, of course, the capital providers. There are debates on the share of the returns that should flow back to each constituent, but by and large, this describes a capitalistic system.

Over time, venture capitalists (VCs) became a necessary component of this system as they proved to be adept at the incredibly difficult dual task of both identifying entrepreneurs and building relationships with those with capital. It remains the job of VCs today to manage relationships with those with capital (Limited Partners) and guide the flow of capital to entrepreneurs at the early stages of their venture creation. In the United States, this form and practice of venture capital investing built cities such as Lowell, Massachusetts (textiles), Pittsburgh, Pennsylvania (steel), Detroit, Michigan (automobiles), Rochester, New York (photography and optics), Houston, Texas (oil and energy), and, more recently, Silicon Valley, California (semiconductors and information technology), among others.

An abridged version of the evolution of venture capital in the United States

The impact of venture capital in the United States brings me to my next point.

Second, venture capital is supposed to (or at least designed to) derisk other investments in an economy. By taking on the most risk in the economy, to create order out of chaos, opacity, and mistrust, venture capital investments trigger the creation of the necessary companies and institutions that can, over time, derisk an economy.

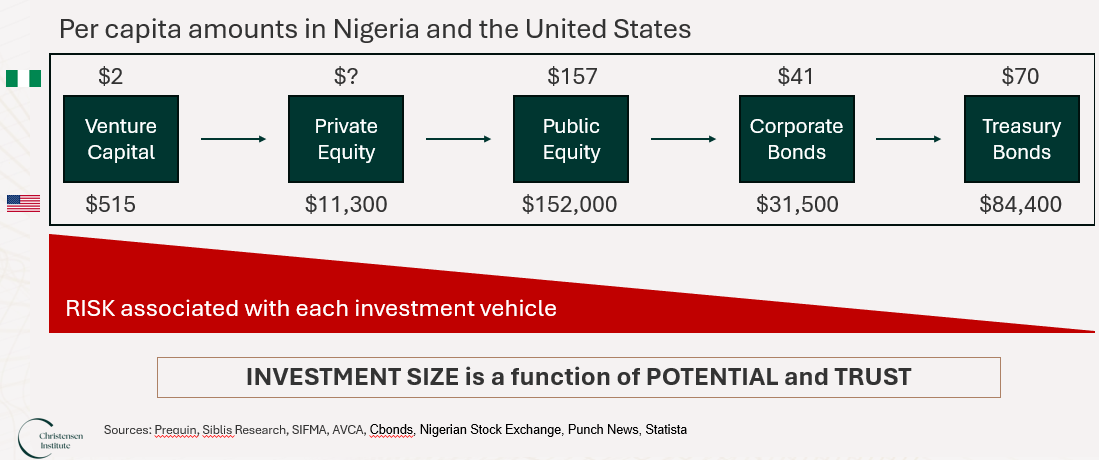

Consider these different financial vehicles in an economy: venture capital, private equity, public equity, corporate bonds, and so on. It is clear that venture capital is the vehicle that can absorb the most amount of risk in an economy. When many venture capital investments create high growth companies that employ thousands of people and create value for millions, the economy begins to stabilize and become more predictable. Follow on capital, by way of growth private equity, venture debt, and public offerings are helpful to further scale the operations of these companies.

The size of investment an economy can attract is a function of the potential the economy offers and the trust investors have in the economy. Successful high growth venture capital firms can demonstrate the potential while also creating the necessary trust. Without this initial venture capital investment in high growth companies, it would be difficult for poor countries to raise follow-on capital. If this happens, the follow-on capital will have to take on the type of risk reserved for venture capital and this could lead to misaligned incentives, misunderstandings with capital providers, and ultimately failed investments.

Size of different financial vehicles in Nigeria and the United States, circa 2023

NOTE: I wasn’t confident in the data I got for private equity so I decided not to include it.

Laurence Rockefeller, pioneering venture capitalist and grandson of John D. Rockefeller said it best, “Venture capital endeavors are not for the impatient, the faint of heart, or the poor loser. Nor are they for widows and orphans or people who cannot afford to lose.”

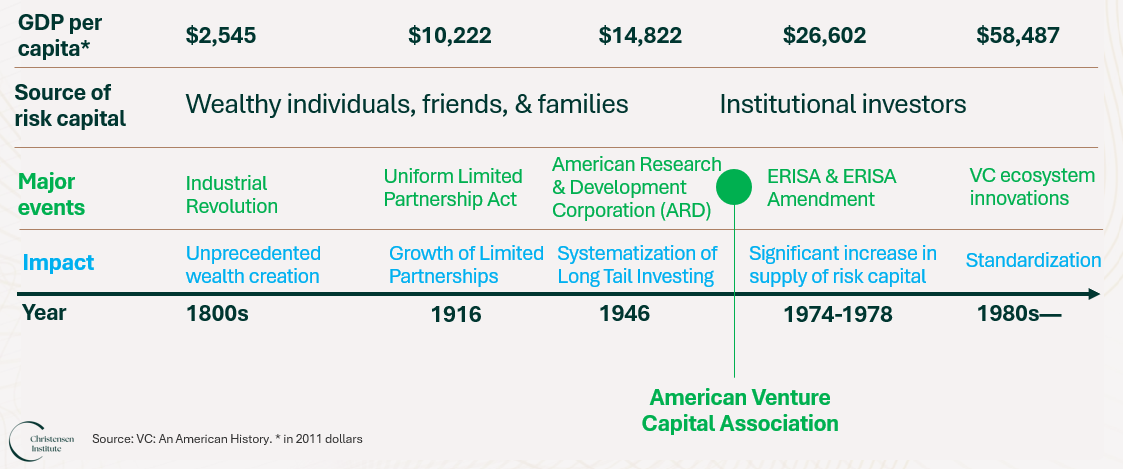

Third, venture capital investors in Africa must learn to work with the government. There are many reasons to outsource the creation of an “enabling environment” to African governments but that would not accelerate African prosperity. Consider how U.S. venture capitalists worked with the government to catalyze the growth of the sector. In 1973, a couple of decades after American Research and Development Corporation (ARD), the first modern style venture capital fund was established, the VC industry created the American Venture Capital Association. This group was responsible for lobbying the U.S. government for risk capital friendly laws that could further galvanize the sector. One such law that was paramount in opening the floodgates of funding to flow to venture capital firms was the Employee Retirement Income Security Act of 1974 (ERISA). ERISA enabled pension funds and other institutional investors to deploy risk capital to venture capital firms.

A very brief history of venture capital in the United States

The outpouring of risk capital led to many other innovations such as, venture debt, mezzanine capital, IPO intermediation, compensation techniques and so on, that have helped standardize and globalize the venture capital industry today.

The implications for venture capital in Africa is that the African Private Equity and Venture Capital Association should have an office in every major African city and capital working with local, state, and federal governments on how to better deploy risk capital to the millions of young and brilliant entrepreneurs on the continent. In addition, general partners of major funds should be spending a portion of their time working with both the government and other ecosystem partners to grow the sector sustainably.

Admittedly, before I attended the Africa Prosperity Summit, I felt that venture capital was important for Africa’s growth but I didn’t think it was pivotal. The more I learn about what venture capital is (risk capital that creates order in a sea of mistrust and opacity), how it helps catalyze the growth of other investment vehicles in economies, and its importance in creating wealth for entrepreneurs, investors, and citizens, the more convinced I become that venture capital is necessary to ignite prosperity in Africa.

A short aside

An incredibly important component that often gets lost or overlooked in the story of development is that of love. Many of the wealthy elite who created the venture capital industry loved their cities, countries, or just loved technology and wanted more people to have access to it. After World War II for instance, it was a sense of civic duty that led many Boston elites to invest in the New England city. Their commitment to Boston led to ARD and ultimately burst forth the modern VC movement after ARD proved that long-tail investing was financially viable.

Efosa serves on the investment committee of Ventures Platform Fund, a pan African venture capital fund dedicated to funding market-creating innovations in Africa.